One of the trickiest parts of advising clients is helping them achieve their goals using assets whose past returns are certain, but whose future returns are not.

Setting expectations is a critical function for FAs to preempt client misbehavior that often derails the most well-thought-out strategy. This is most often the case when expected returns fail to materialize, creating doubts about the strategy and the advisors who recommended them.

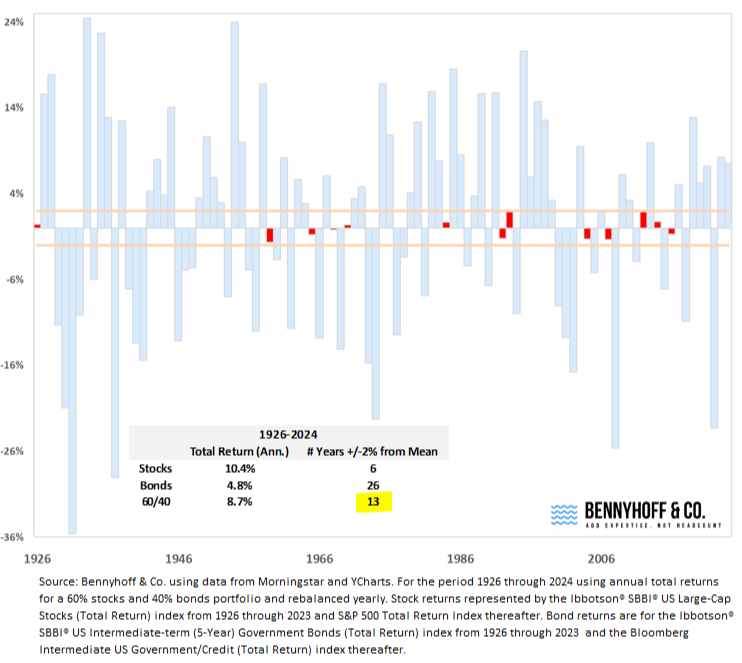

The chart below illustrates the historical return deviations of of a 60/40 portfolio relative to its long run mean return of 8.7% (yes, I know the mean varied over that time... throw me a bone for simplification).

What is often overlooked is the value of asset allocation in dealing with this challenge. As the table shows, returns from stocks, bonds, and a 60/40 portfolio are rarely 'normal' - that is, rarely deliver returns close to their long run averages (here, defined as within 2% +/- of their mean and represented by the orange lines in the chart).

However, when you consider that stocks AND bonds only delivered 'normal' returns in the same year TWICE during the period, then I think the 13 times the 60/40 portfolio did so look more remarkable.

Of course, past returns aren't prologue, but maybe asset allocation deserves a little more credit for promoting better client behavior, not just ensuring that all our eggs aren't in one basket.